The Home Loan Process

Demystifying Home Loans

If you haven’t experienced it before, the home loan process can feel overwhelming, but our agents will help you stay informed throughout the process, from pre-approval to closing. The first thing to do is consult with a mortgage specialist (or two). If you don’t already have someone in mind, we partner with some of the best lenders in the industry, and we’d be happy to introduce you, so you’ll be taken care of.

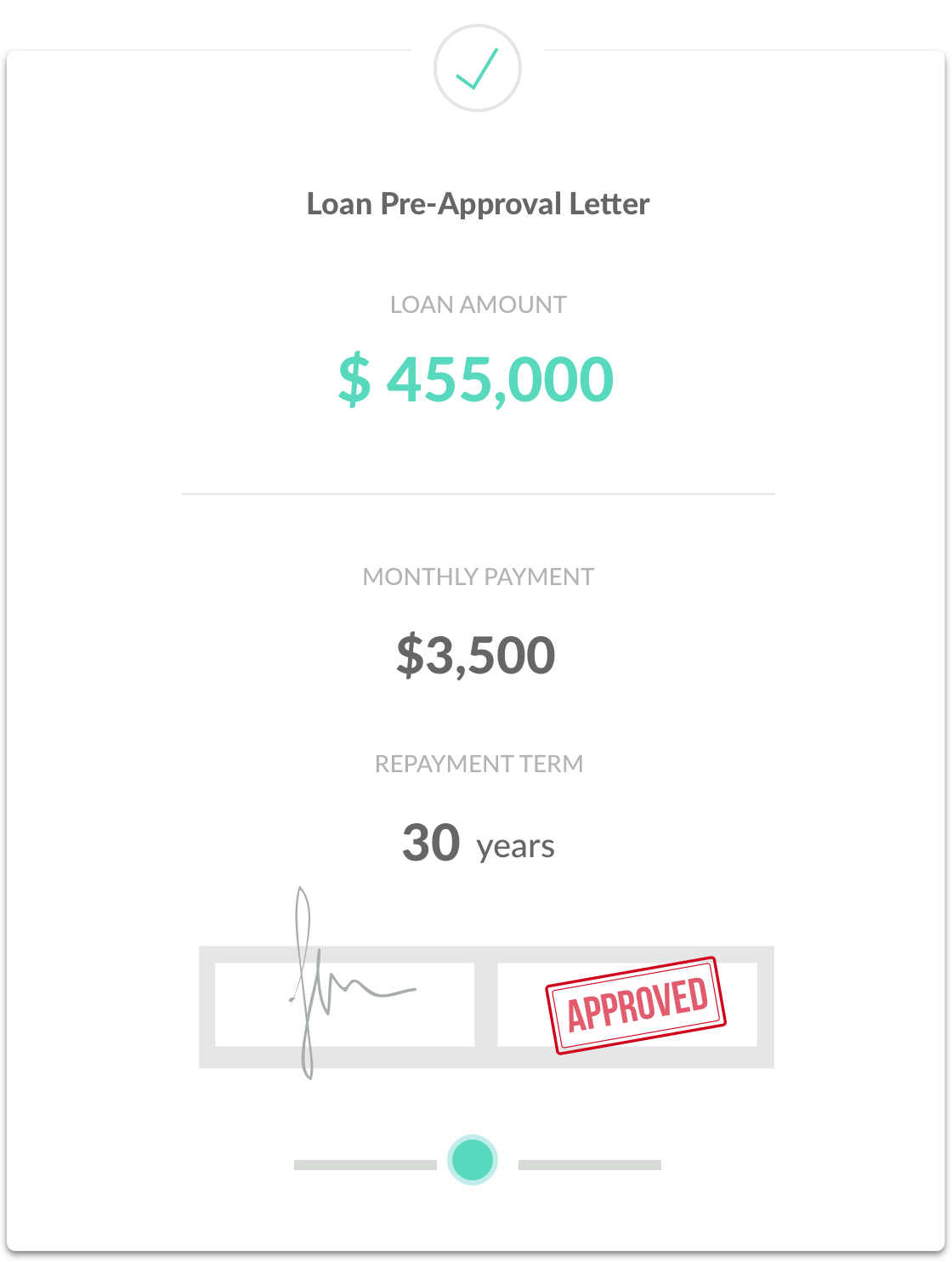

Get Pre-Approval

Before you start looking for a home to buy, it’s a good idea to meet with your Loan Officer to get pre-approved for a loan amount. At this stage, the lender gathers information about income, assets and debts of the borrower (you) to determine how much house you may be able to afford. This includes a credit report, W-2 forms, pay stubs, Federal Tax Returns and recent bank statements. There are a variety of different loan programs, so make sure to get pre-qualification for the specific programs that best suit your needs.

finance with

Movement Mortgage

Matina Geanopoulos

Loan Officer

NMLS ID # 1438121

State License #MA-MLO1438121, CT-LO-1438121

- 413-351-1310

- matina.g@movement.com

Welcome to our stress-free, easy-to-understand mortgage process. As your loan officer, backed by Movement Mortgage’s teams and resources, your perception of the homebuying process will be changed for the better. Whether you’re buying, selling, refinancing or building your dream home, there’s a lot riding on your choice in a loan professional. I have the knowledge and experience to help you explore financing options in a way that’s simple and straightforward. Together, let’s take a look at what you can qualify for.

Let's Get Started

finance with

First World Mortgage

Denise Lanouette

Mortgage Consultant

NMLS ID # 1280257

Company NMLS ID # 2643

- 860-944-0280

- denise@firstworld.com

- 860-200-8138

Denise Lanouette has been in the lending industry for over a decade. She learned the process from the ground up, having started on the operations side before shifting to origination. For years she was assisting multiple top producers, which offered her opportunities to learn the process and the business environment. She came to define what kind of business she wanted to run for herself, which drove her to eventually become an originator! Denise has a degree in Psychology. As such, the personal relationships and help she provides as a loan officer is what she values most. She knows what it takes to make a loan successful. When she gives a loan approval, it is solid as a rock!

Let's Get StartedWe Help You Get The Best Loan

Start The Process

We’ll help you find the best local loan officer to get you competitive rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with a lender today!

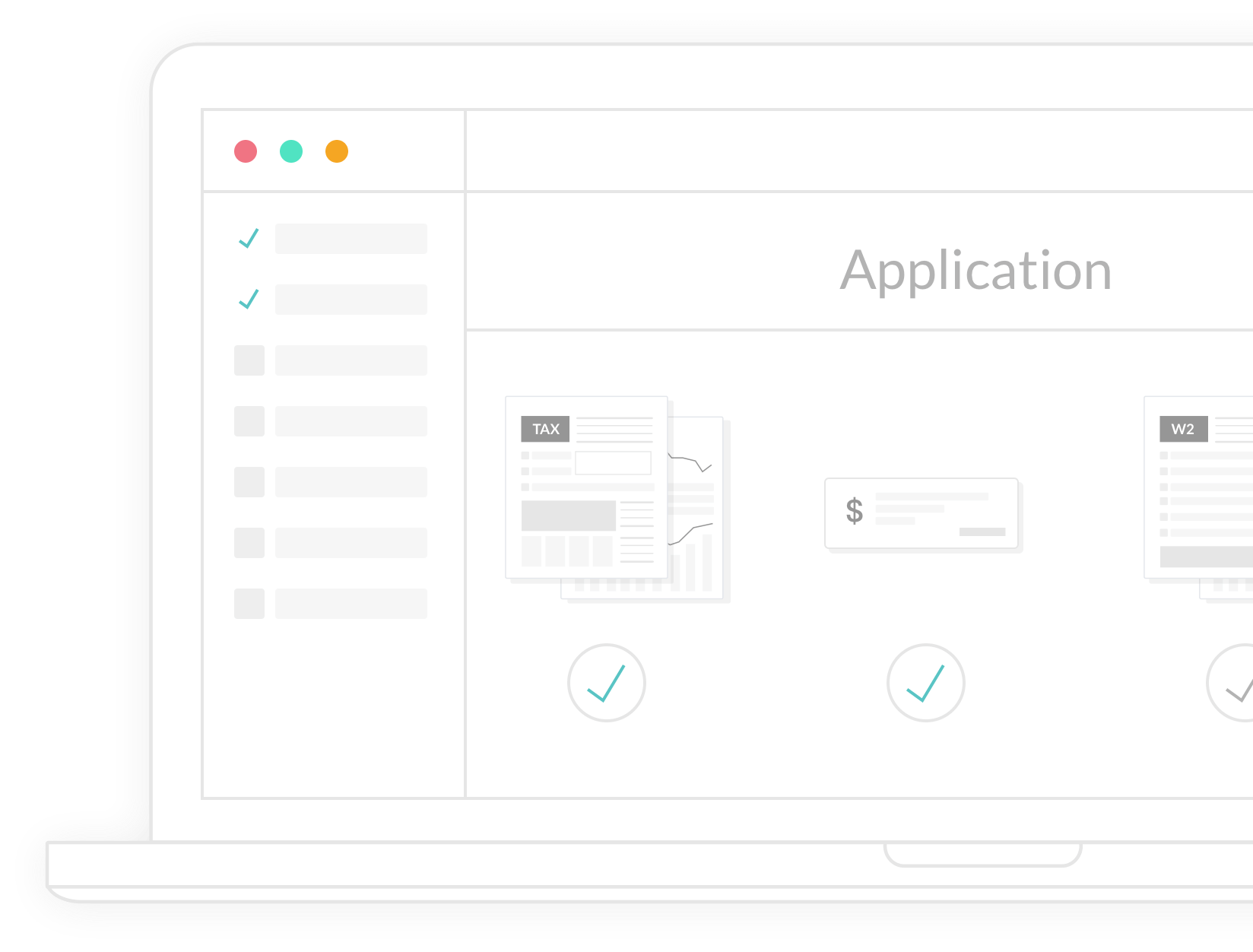

Application & Processing

What happens when a loan goes "live"

When you find property you’re ready to buy, your lender will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. The application is submitted to processing, where the documents are reviewed and appraisals and title examination are ordered. Then the loan is sent to an underwriter, who reviews and approves the entire loan if it meets compliance.

Closing

Signing and Finalizing the deal

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. Once your loan is approved, don’t forget to set up homeowners insurance. Your documents will be sent to the title company, where you’ll sign for the new home and pay any remaining costs. Then the loan is recorded and you get the keys. Congratulations, happy homeowner!